Main Reasons Why Your Credit Score May Have Dropped

15th Jul 2024

Finding out about credit scores and understanding your numbers often feels like getting through a maze, where various financial decisions and behaviours influence every turn. The world of credit scoring and lending is complex, and each lender has its own criteria about who it wants to lend to. However, what is true is that people who have higher credit scores have access to a wider range of credit options, at better prices, than people with lower credit scores.

Credit Score Weighting

Your credit score is made up from five categories with different levels of importance, which look at different aspects of your financial behaviour. These are:

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

Common Reasons for Credit Score Drops

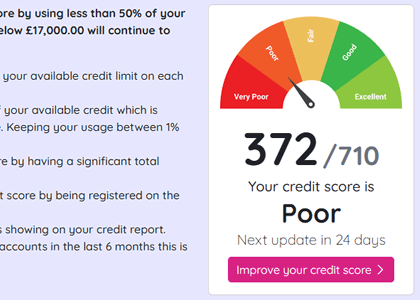

Credit scores do go up and down over time, and small changes are nothing to worry about. Knowing the factors which affect your credit score gives you the ability to do something about the negative changes. Some of the most common reasons why you might see your credit score going down are:

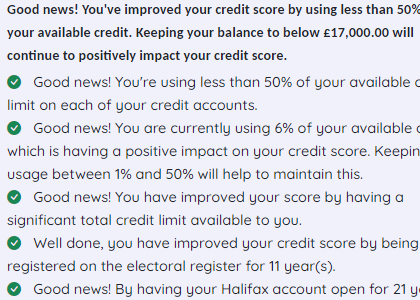

- Late or missing payments: Payment history is one of the most important factors in calculating your credit score as it’s a seen as a key measure of financial responsibility. Try to keep on top of paying bills on time.

- Recent credit applications: Each hard search for a credit application can slightly reduce credit scores and may signal financial instability.

- Increased credit utilisation: A sudden change in habits around the way you use credit can ring alarm bells as it might be a sign of financial insecurity.

- Decreased credit limits: If your credit card company suddenly reduces the limit on a credit account, this can also affect your credit score negatively.

- Closed credit cards: Closing a credit card account reduces overall available credit and may shorten credit history, affecting credit scores.

- Inaccurate information on credit reports: Mistakes on credit reports, such as incorrect late payments or accounts opened through identity theft, can unjustifiably lower credit scores.

Strategies to Improve Credit Scores

There are lots of things you can do to improve your credit score by showing you are a responsible borrower. As discussed, the most important thing you can do is to make sure your bills are paid every month, with no defaults or missed payments. Keep your old credit accounts open and active, as this will show that you are not using all of your available credit. Having accounts with a long history will also go in your favour. Try to keep any new applications for credit to a minimum, using soft searches to assess your likelihood of being accepted before going ahead and making a firm application. Finally, get into the habit of checking your credit report regularly, and flag up any mistakes to the credit referencing agency for correction. No need to be obsessive over it though, checking every fortnight or once a month is ideal.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

An Independent View Of Your Credit Score

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.