What is a Credit Utilisation Ratio

8th Jul 2024

When the credit referencing agencies calculate your credit score, there are numerous factors which they take into consideration. One of these factors is your credit utilisation ratio, which indicates the percentage of your available credit that you're currently using. Unlike other factors which affect your credit score such as missed payments, your credit utilisation ratio is a bit harder to work out. Understanding your credit utilisation ratio is seen as important by lenders as it reflects your credit usage habits and your reliability as a borrower. A high ratio could adversely affect your credit score, while maintaining a 0% ratio might not provide evidence of responsible credit usage.

Working Out Your Credit Utilisation Ratio

Your credit utilisation ratio looks at the proportion of your total available credit that you're using. For instance, if you only have one credit card with a £1,000 limit and you have a balance of £200, your utilisation ratio would be 20%. Most people however have more than one credit card, so to find out your overall credit utilisation ratio, you have to add up all available credit across the different cards, and the balance on them all to determine the percentage used.

What is a Good Credit Utilisation Ratio?

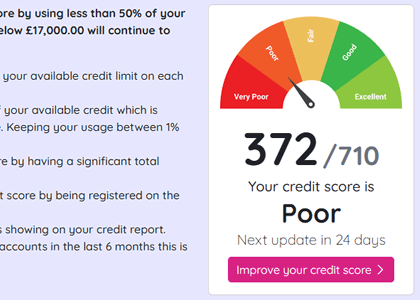

Every lender differs in the importance they put on credit utilisation ratio when compared with other factors. They also each have their own ideas about what is an acceptable ratio. In general terms though, credit utilisation ratios are graded as following:

- Over 75%: Using more than 75% of your credit limit may raise concerns for lenders, as it can be an indication of potential financial strain or difficulties.

- 50% to 75%: Using over half of your available credit might impact your credit score negatively, though to a lesser extent than exceeding 75%.

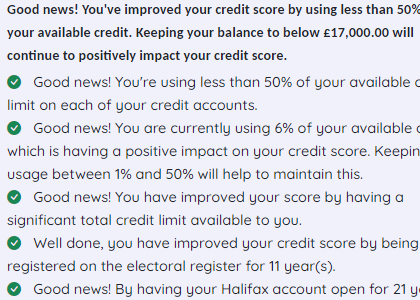

- Under 30%: Keeping your utilisation below 30% is advisable, with some agencies suggesting under 20% for further credit score improvement.

While having a 0% utilisation ratio might seem the best possible scenario, it could actually have the opposite effect. Not using any of your available credit means you are not giving lenders any information to form a perception of you as a borrower. Lenders prefer evidence of good credit management, so it’s actually better to make a point of using a credit card regularly and paying it off every month to build your reputation.

If you think your credit utilisation is on the high side, focus on paying down existing debt. Transferring debt to a 0% balance transfer card to reduce interest costs temporarily can help you pay debt off even quicker. Remember that once you have cleared all the debt on one credit card, don’t be tempted to close the account as that will have a negative impact on the credit ratio as you will be using a higher percentage over time. Track your credit score over time to see what effect your actions are having, bearing in mind that there are lots of factors which all combine to determine your overall score.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

An Independent View Of Your Credit Score

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.