Top Tips for Boosting your Mortgage Chances

6th Jan 2024

Securing a mortgage deal for a new property can feel like a daunting task, especially in the middle of a cost-of-living crisis and changing interest rates. However, there are some tips and trips which can help to improve your chances of obtaining a good deal, however good your credit rating is. If you understand about how the mortgage market works, and how your credit rating affects your prospects of getting a good deal.

Lender Expectations Vary

Each mortgage lender or bank has its own criteria for approving mortgages. All will look at factors such as the loan amount, the size of deposit which you have, whether you are employed full time or on a temporary contract, what else you spend your income on, and what other debt you have. Each lender rank factors in a different way, so being accepted by one lender doesn’t automatically mean you will be accepted by others.

Understand Your Credit Report

Before you start the process of trying to find a mortgage, study your credit report. Lenders will be looking for proof that you have a good repayment history, with no county court judgements, late payments and high levels of debt. If when checking your credit report you find mistakes, speak to the credit reference agencies to have them fixed. They will ask for evidence to prove the error but should correct mistakes quickly. Get into the habit of checking your credit report every month to make sure no new errors appear.

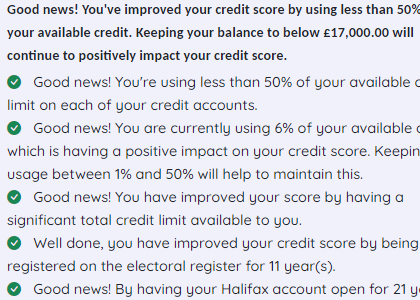

Register to Vote

Being on the electoral register is one of the most important things you can do, as lenders use this data for identity verification. You can register to vote online, and there is no charge. If you are not eligible to vote, ask the reference agencies to include a notice of correction on your file, along with alternative proofs of address and identification.

Manage Your Available Credit

The way in which you use the credit available to you should paint a picture of you as a responsible borrower. Aim for a debt level equivalent to 25% of available credit to present a favourable image to lenders. Some lenders are starting to factor in buy now, pay later commitments, so be mindful of their impact if you used this form of credit.

Limit Credit Applications

Avoid applying for additional credit in the months leading up to a mortgage application. Multiple credit checks within a short timeframe can damage your credit score and stop you getting a mortgage. A six-month gap is advisable, especially for payday loans.

Think About Getting a Mortgage Agreement in Principle (AIP)

A Mortgage AIP is a conditional offer indicating the likelihood of being accepted based on income and credit file checks. This is similar to other soft credit searches and won’t leave a negative mark on your credit report. Once you have an agreement in principle, you will know how much you can expect to be allowed to borrow when you go ahead and make a formal application.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

An Independent View Of Your Credit Score

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.