What is a Mortgage Decision in Principle?

17th Sep 2024

A mortgage decision in principle, also sometimes referred to as a DIP, is a crucial first step when buying your home. It provides an official estimate of how much you can borrow. It can give you confidence, and show sellers that you're serious. Often, estate agents will want to see your DIP before allowing you to view properties. Banks consider a wide range of factors when looking at issuing a DIP, including your credit score, income and outgoings. What do you need to know about getting a decision in principle if you are thinking about stepping onto the property ladder?

Why a Decision in Principle is Key

A decision in principle is incredibly valuable to both you as a buyer, and to estate agents and vendors. It provides an official estimate of your borrowing capacity and indicates to sellers that you're a serious buyer. The process is straightforward and can be completed online in just 10 minutes in many cases. As you are only applying for an estimate of what you might be able to borrow, a DIP doesn’t count as a hard credit application, only a soft search. This means that it will not affect your credit score.

To get a DIP, you'll need to provide financial details for yourself and anyone you're buying with, an idea of the type of property you want, and the amount you plan to borrow. This can usually be done online through the bank or building society which you are considering using for your full mortgage application.

Transitioning to a Full Mortgage Application

After receiving a DIP, it remains valid for 30 days, during which time you can use it to make offers on properties. If you see a property you really want to buy and have an offer accepted, then you will have to proceed to making a full mortgage application. This is a hard credit search and any lender will look at a wide range of factors when deciding whether to lend, such as your income, credit history, employment status, value of the property you are buying, and your other outgoings. You will need to provide a wide range of documents to your lender, including proof of identity such as passport or driving licence, payslips from your employer, bank statements and information about the property you want to buy.

Get Your Credit in Shape for a Mortgage Application

Responsible lending is one of the current industry buzzwords and this means that whatever the bank, you can expect them to ask lots of questions and ask for lots of original documents to support your case. Getting all of the documents together can take some time, so start the process as quickly as you can. Most of it will probably be done online, but you still may have to make an appointment to go into the bank or lawyer’s office to sign documents in person. Properties are in high demand in many areas of the country, so don’t risk losing out by missing deadlines.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

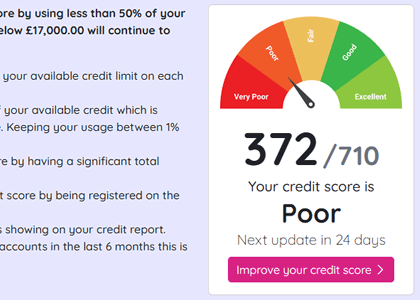

An Independent View Of Your Credit Score

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

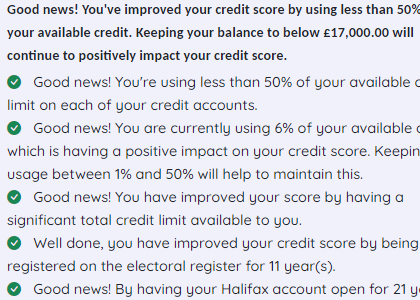

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.