My Card Credit Limit Is Too Low!

12th Jan 2024

When you initially get approved for a new credit card you will probably at first be delighted. However, realising that you’ve been given a credit limit that falls short of what you were expecting for your intended purchases or debt transfers can be disappointing. It might be that your credit score isn’t as good as it could be. Don’t cancel the card out of frustration, tempting as it might be. There are some things you can do to deal with the situation.

Understanding Credit Limits

When you get any new credit card, it comes with a predefined credit limit, which sets the maximum amount the lender is willing to give you. Credit limits in the UK typically range from £3,000 to £4,000 on average, but if you have a lower income or poor credit history your limit might be as low as £200. On the other hand, higher earners with a positive credit history might be given a limit exceeding £10,000.

Why Lenders Set Low Credit Limits

Lenders judge credit applications based on various factors such as outstanding debts, available credit, repayment history, and how many other lines of credit you have recently applied for. Recent years have seen tightened credit practices, leading to reduced credit limits. This happened after the credit crunch of 2008, where banks were heavily criticised for giving out too much money to people who had no hope of ever paying it all back.

Requesting a Credit Limit Increase

If you are not happy with your credit limit, you could try asking the credit card company if they will increase it. However, they are within their rights to refuse, and the likelihood of success often improves after having the card for a few months and proving that you are a good customer. Many credit card companies will increase your credit limit each year you remain a customer with them, and having a positive credit history with one company should make it easier to get a different credit card with another. Credit card companies generally will not share their reasons for setting a particular credit limit, and call centre staff may not have the ability to increase you limit even if you call them up and ask.

Why Cancelling Isn't the Solution

When you get a new credit card and find the credit limit isn’t what you’d hoped for, it can be tempting to cancel the agreement and cut up the card. However, cancelling the card impulsively can have drawbacks. Firstly, applying for another credit card straight away could have a negative impact on your credit report, as the reference agencies will not be aware that you are not planning on using the first card you applied for. Also, it takes time to cancel the first card and get a new one. It may be better just to start using the card with the lower limit, with a view to delaying spending until the limit increases, or to ask for an increase in a few months.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

An Independent View Of Your Credit Score

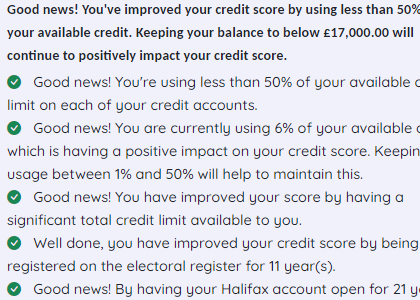

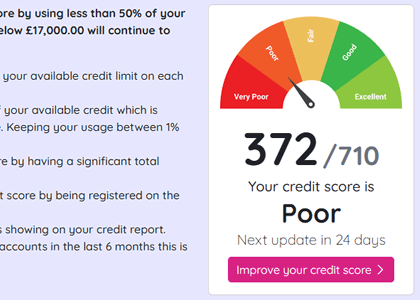

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.