7 Things to Do Before You Apply for a Mortgage

24th Jun 2024

Would you lend money to a friend if you thought you didn’t stand much chance of ever getting it back? Mortgage lenders make decisions on the same basis, and as they don’t know you on a personal level, they will look at your financial history and credit report when deciding whether to lend you the money you have asked for. Applying for a mortgage can be a stressful time, and if you do some preparation up front, it should make the whole process run more smoothly.

1. Understand Lenders' Criteria:

Take some time to work out what sort of person is the lenders’ ideal borrower. Each lender is slightly different when it comes to their target customer. Lenders don’t just look at your overall income, but also weight that up against borrowing amount, how much you have to put down as a deposit, employment status, credit rating, and existing debts. They also consider affordability and look at how you might be able to afford repayments if your income changes.

2. Assess Your Financial Health:

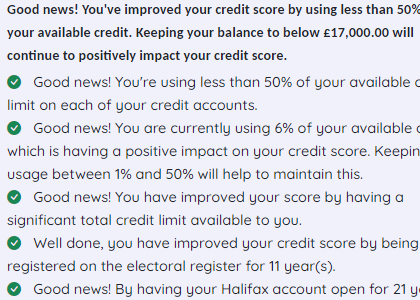

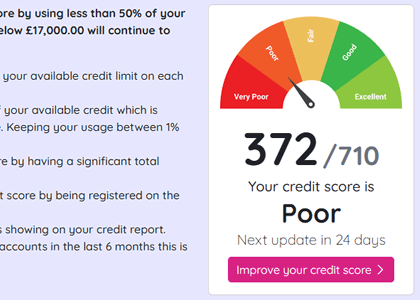

Before applying for a mortgage, try to reduce or eliminate debts to leave more available funds for monthly repayments. Avoid maxing out credit cards or relying heavily on overdrafts, as it may suggest financial strain and make lenders wary about lending to you. Monitor your credit score over time to make sure the numbers are headed in the right direction.

3. Establish Creditworthiness:

Lenders will look at credit reports for details of your repayment history. Regularly monitor your credit score through reputable providers to make sure there is nothing on there which could raise red flags about your financial behaviour. Any mistakes should be raised with the agency for correction.

4. Register on the Electoral Roll:

Being registered to vote serves as identity proof for some lenders, and if you are not listed on the register, you’ll face refusal at the first hurdle. Register online at www.gov.uk/electoral-register for free if you’re not a registered voter already.

5. Prepare Necessary Documents:

Gather essential paperwork, including bank statements, pay slips, proof of commissions or bonuses, tax returns, P60 form, savings account statements, identity documents or utility bills. Original copies may be required, so plan accordingly as you might have to ask for hard copies to be sent in the post.

6. Accuracy Matters:

Complete paperwork carefully to avoid delays or resubmissions. Always provide precise income details, full name including middle names, disclose all debts, accurately list address history, and provide honest expenditure details. If you are using a mortgage broker, they will help you present the best information to lenders.

7. Obtain a Decision in Principle (DIP):

A DIP serves as a preliminary check indicating potential lending approval. While not definitive, it provides insight into potential borrowing limits and is what most estate agents will expect you to have when making offers on property. Once your offer has been accepted, you can then go ahead and make a firm application for the funds.

Don't risk missing

something important

Access a comprehensive credit report

that includes detailed data from TransUnion

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.

See How You Score

See How You Score

An Independent View Of Your Credit Score

Lenders typically use their own systems to calculate your Credit Score based on the information in your Credit Report, often checking with one or more Credit Reference Agencies. Your Credit Check Online Credit Score is derived from all the Credit Report information we gather from TransUnion, helping you understand how you might be assessed when applying for credit.

Understand What is Affecting Your Credit Score

Quickly see how the details in your Credit Report influence your Credit Check Online Credit Score, both positively and negatively. This clear overview helps you identify areas for improvement and better understand the factors that lenders consider when assessing your creditworthiness.

View your credit score for only £1.95.

You can view it for 1 month, after which it will be £14.95 per month unless cancelled.